Today (April 14th, 2015) Paul Hilal from Pershing Square came to speak during the “Value Investing with Legends Class.” In his introduction of Paul, Professor Big G (Bruce Greenwald) said this, “The public face of Paul Hilal’s fund is Bill Ackman, the talent to a large extent is standing in front of you.”

Paul certainly lived up to the “generous” introduction. He gave a very meaty lecture, full of insights, important life lessons, juicy and entertaining details of Pershing’s activist campaign against Canadian Pacific Railway in 2012. Paul came across as personable, candid, and grounded. But underneath all these qualities, it was clear that he would not hesitate to turn ruthless (I think all successful business people have this quality more or less) when it comes to sticking to his principles/beliefs and driving value from his investment ideas. Many of the lessons he conveyed are not just about investing, but more importantly about life, about being a principled person, and about life in business. There are lessons to be drawn whether you are an investor, a consultant, a general manager, or a banker. It is learnings like this that makes me feel lucky to be at Columbia Business School.

Below are my key takeaways from the lecture. Some of these may sound cliche but they are very true and fundamental to the governing of one’s life and career. Paul conveyed these with true life stories and great passion:

1. Paul Hilal – Background and Bio:

48 soon to be 49

48 soon to be 49- Dad is a radiology professor at Columbia Medical School

- Harvard undergraduate, intended to be a research scientist but realized it was not his goal. After colleague re-enrolled at Columbia for a JD-MBA joint degree program to reinvent himself, spent 3rd summer in school in investment banking at Credit Suisse, after school ended up taking a job at an M&A boutique (Broadview) in 1992, Broadview specialized in Info Tech. Experience offered a top-down view of industries, strategies, demystified the executive suite, they are also humans

- May 1997, met a charismatic guy who just raised $200mm, wanted Paul to be the internet & tech guy. Took a 7 months sabbatical. After coming back, left in three weeks, this was Rajaratnam.

- Then joined his brother Peter in a small fund with a broad mandate

- Took the opportunity to turnaround a failing tech company

- In 2005, Bill Ackman (Harvard roommate) approached him then the rest is history

2. Life Lessons

- Integrity, principle, and moral compass

- You will find yourself in situations that is very uncomfortable ethically. It’s easy to look the other way and try to rationalize. The mere fact that you made it to Columbia means you are smart and hardworking, and you don’t need to cheat to succeed. This should be an easy moral choice. For people who are struggling, the choice may be harder and the story is different. Nonetheless, it never pays.

- Paul’s example: 16 years ago Paul took a job with Raj Rajaratnam and quit in 3 weeks after he realized shady things were going on at the firm and the man lacked utter moral compass. And he was right, 10 years later, Rajaratnam was arrested and sentenced to 11 years for insider trading.

- Take advantage of life experiences

- It’s important to take advantage of life experiences as an opportunity to learn, grow, and mint memories when you are still in a flexible situation (e.g. if you have 3 months before start working, seize it and go travel)

- Paul’s example: after he left a successful run in banking at Broadview and had a 7-months window before officially joining Raj Rajaratnam’s hedge fund Galleon, he literally travelled around the world. Not everyone could afford to do this, but when there is such opportunity, seize it and you will not regret.

- Take calculated risks, you can afford to tolerate more risks than you think

- People are sub-optimally risk averse by nature, but life is more healing than you think. There will be a time in your career that some unusual opportunities arise, think carefully but trust your instincts, take calculated risks. If you conduct yourself with great integrity for life and maintain close relationship with people who know you, you can afford to tolerate more risk than you think. Even if you fail, with integrity, being hardworking, and being smart, there will be people willing to work with you.

- Paul’s example: he took the opportunity to turnaround a failing tech company in California and sold the company for 4 times his investment a year later

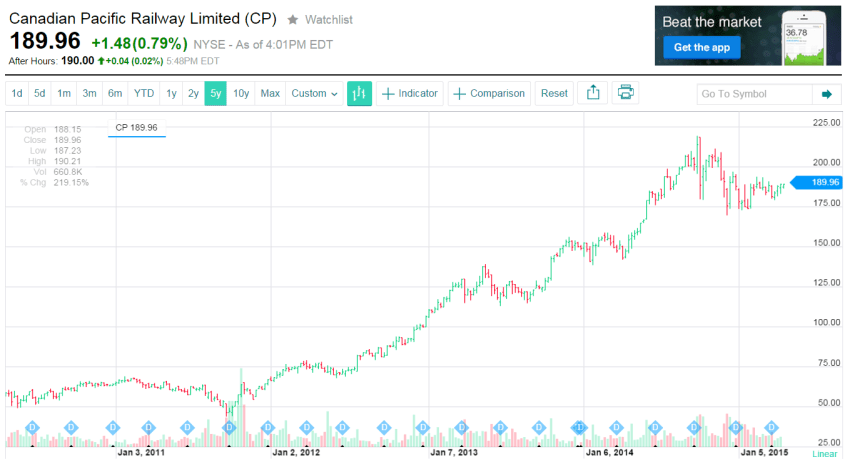

3. Investment Lesson – Activist Campaign against Canadian Pacific Railway

In July 2011, through conversation with his younger brother, Paul learned that there is an under-performing Canadian railway company that investors have lost a lot of money on and have been complaining about, so add the sector to his watching list. By early August, decided to focus on looking at the sector.

- Specialist vs. generalist – there is a lot of value in specialization, but there is also a lot of value in being a generalist. You approach a topic with fresh eyes, and not prejudiced by all the assumptions that people who have looked at the sector for 20 years had, and you see things in a different way. Paul started out focusing on info tech and biz services at Pershing then branched out into other sectors.

- Business due diligence – Canadian Pacific vs. Canadian National

- Businesses and operating environment (similar freight mix, same weather, networks overlap etc.) are extremely similar but EBIT margins are drastically different, CN (40%) and CP (18%), and U.S. railway companies (30%), WHY?

- Investment community has accepted on face value why CA Pacific could not achieve the same margin, where by management cited the following “structural challenges” to explain away the difference:

- Weather is different

- Freight mix is different

- CP’s tracks are running on steeper grades, the tracks are also curvier

- After deeper study, the seemingly reasonable “structural challenges” on paper actually do not stand up to the reality.

- Tracks are steeper in certain areas, but not by much, and only along a small fraction of the network

- Curviness is hard to see

- Most tracks overlap in similar weather system

- Then there are other metrics that cannot be explained by the “structural challenges,” such as freight idle time. This indicates that there is structural mismanagement of the company

- . Cultural due diligence

- Spoke with alumnus from CA Pacific (operating ppl at mid and lower-mid level), business partners, and clients. The findings are that CP has a culture of slackers and CN are the go-getters.

After the investigation, the key insight is that the solution is to fix the culture, fix the management, this could be done without much incremental capital

- Find a change agent

- Lesson: It’s ok and don’t be afraid to cold call people for help. Paul cold called Hunter Harrison out of the blue to learn about the railway industry. Hunter is the former CEO of Canadian National Railway, a turnaround legend that fixed two railroad companies, and had retired 18 months prior. Hunter did not know Paul before but spent two and half hour talking to him (Paul’s intelligence, persona, and his status certainly helped I think).

- Paul didn’t tell Hunter what he was looking for, didn’t want Hunter to know he was interested in CP, didn’t want Hunter to know he had a thesis, and did not want to bias Hunter’s view, as people (no matter how smart they are) have a tendency to tell you what you would like to hear.

- Saw Hunter’s knowledge, insights, communication skills, and passion for railroad continued to burn bright, knew this is the guy to turnaround the company

- On September 27th 2011, persuaded Hunter to come out of retirement

In the meanwhile, Canadian Pacific’s stock price continued to drop. At $47 per share, before fully confirming the thesis, decided that the price was too cheap, started vacuuming up 20-30% of daily volume for two weeks, drove the share price from $46 to $66 and eventually bought 14% of the company (target price based on conservative thesis is $150+ in three year). Typically people say you drove up the stock price then should wait for it to pull back, but in this case the thesis was so powerful. The next step is to effect the changes.

“Key lesson – Have conviction and convey that, you need to underwrite your thesis both internally and publicly. As an activist, the last thing you want to do is go out, promise THIS, be given the keys to the company, then deliver THAT. Then you will never be given the keys again as the public will think you are overly promotional, your analysis is not rigorous. So you always want to under-promise and over-deliver so that you could set yourself up for success in the next activist campaign.”

- Deal with a powerful board that is resistant to change

- Faced a high profile board comprised of Canada’s political and business elites. Canadian Pacific is the crown jewel of the second largest company in Canada, and a national symbol. Being on the board is being in the winners’ circle. The conversation is highly emotionally and politically charged, but the rule is to be as simple and as direct as possible.

- In November 2011, meeting with the board took place in a private room at a private airport. Bill and Paul tried to be polite, wanted to use the directors’ ego as a tailwind as opposed to a headwind (e.g. instead of saying there are the under-performance, say here are the opportunities). Pershing’s key proposals are:

- A dignified and lucrative exit for the incumbent CEO (Fred Green). Would tell the public that Fred lured Hunter out of retirement, and he himself would retire into the sunset with a large exit package (Sounds reasonable, hum?).

- Current board members to stay and oversee the turnaround and take the glory and the credit

- In return, expand the board (not replacing anyone) to include Pershing’s nominees, hire Hunter as the CEO for the turnaround

- But the board meeting was disappointing, the incumbents rejected all the proposed changes and now Pershing faced three options below. Pershing would always choose three and would always go into a meeting with the board assuming the conversation would revert to option three (proxy fight is expensive, need to incorporate into IRR calculation):

- Plead, plead, and continue to plead for change

- Sell stock and walk away

- Go to war (proxy fight) – “clearly we have a disagreement about what’s in the best interest of the company, that’s ok, but let’s let the shareholders decide what’s in the best interest of the company. Now we will take our ideas and present different visions and give the owner a chance to pick different representatives on the board. They can chose who they like, you or us.”

“Key Lesson: Come to the negotiation table with a gun, but don’t put the gun on the table unless you plan to use it. The proxy fight is Pershing’s nuclear weapon in this case.”

Pershing told the board that they would rent the largest hall in Canada, invite everyone (buy-side & sell-side), and lay out in hundreds pages of facts about the underperformance of the company. The board either did not believe Pershing would do it or they would screw up in the process. In the next two weeks there was a little back and forth where the board offered to add one Pershing nominee to the board, but one seat would affect nothing. So the fight went to the shareholders.

- Present a powerful argument to shareholders

- On Feb 6th 2012, held a town hall meeting with shareholders (350 ppl showed up and 1000+ tuned in for webcast). This was a major event as Pershing was going after a board that had been described as Canada’s golden board.

- Presented shareholders with thorough analysis and powerful argument that not only presented facts, but also disabled the current Board’s counter-argument and ability to fight back by raising questions about their credibility.

- The end result is that Pershing asked for seven seats and won all of them with 94% vote from shareholder. The rest is history.

Canadian Pacific 5-Year Stock Price Chart:

—

Zong Z. Peng, CFA

MBA Candidate, Class ’15

Email: ZPeng15@gsb.columbia.edu

Linkedin: http://www.linkedin.com/in/zongpeng